|

amortization.com Ltd. 905-639-0374

|

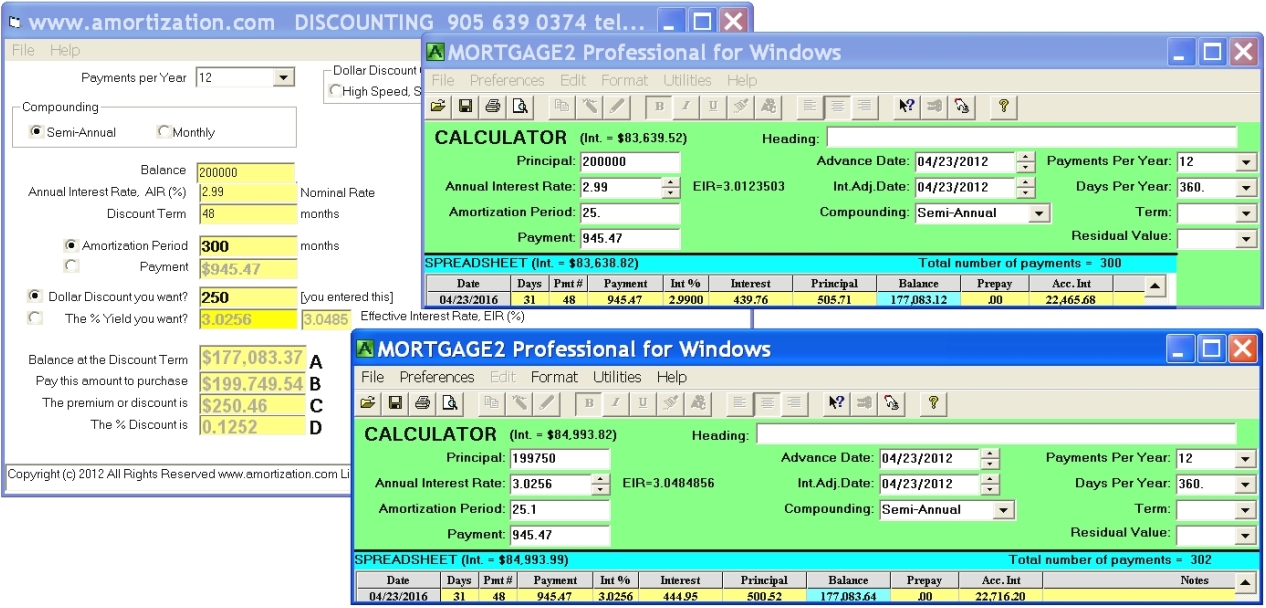

A major Canadian Bank has been advertising a mortgage, using an example, a $200,000 mortgage with a four year term rate of 2.99% and a “processing fee” of $250. In the squint print at the bottom of the newspaper advertisement the Bank states an APR of 3.03%. The 3.03% is a result of the up front $250 processing fee the borrower must pay the bank. The 3.03% is called the APR which is the cost of borrowing. What does that 3.03% actually mean? The explanation depends upon your perspective. It means different things to different people. To a mortgage broker it could mean that this 4 year 2.99%, $200,000 mortgage was sold to another person at a discount for $199,750 and that new person is therefore receiving a rate of 3.03%. To a home owner it means the Bank only advanced you $199,750 and therefore your interest rate in actuality is 3.03% because you are making the monthly payments for a $200,000 mortgage even though you only received an advance of $199,750. Lenders by law in Ontario must quote this 3.03% because it is called the cost of borrowing. The purpose of the APR is to inform the borrower the up front fees increase your interest rate. The proof is in comparing the balance owing after 48 months using the same monthly payments (cash flow). A rate of 2.99% with a PV of $200,000 vs a rate of 3.026% with a PV of $199,750 the balance owing is the same after 48 months in this example. The DISCOUNTING selection in the MENU of my MORTGAGE2 PRO software will quickly and easily calculate the APR to more decimal places and is shown along with the two amortization schedules in this SCREEN CAPTURE. After 48 months the two identical cash flows give rise to approximately the same balance owing, $177,083.12 vs $177,083.64 The difference of 52 cents is because of the incremental rate guess used internally in the DISCOUNT software. No Bank in Canada quotes more than 2 decimal places in their annual interest rates so the DISCOUNTING answer is good enough in practical terms. Internally the DISCOUNTING software could have increased the guess by smaller steps thus getting closer than 52 cents, but then the calculation would not be instantaneous. What the DISCOUNTING software is doing is as follows. Subtract the $250 processing fee from the $200,000 for a Principal of $199,750. Then guess an interest rate that is greater than 2.99% so that we can still make the same monthly payments ($945.47) and end up with the same balance owing after 48 months. My software’s more accurate 3.0256% is shown in the Bank’s newspaper advertisement as 3.03% and is called the APR or the cost of borrowing. The good news is the APR in Canada and the USA are now compatible and thus both mean the same thing, that is, the impact on the nominal interest rate you are being charged due to discounting or because of upfront fees. All of the upfront fees that are legally allowed can also be lumped in with this processing fee to arrive at the APR. The bad news is that the government of Ontario passed confusing mortgage legislation in 2006 and introduced a lot of confusion in the industry. Shown below, is The Brokerages, Lenders and Administrators Act, 2006, ONTARIO REGULATION 191/08, COST OF BORROWING AND DISCLOSURE TO BORROWERS. APR = (C / T x P) x 100 “APR” is the annual percentage rate cost of borrowing, The Ontario government’s APR equation completely ignores the time value of money (aka present value future value) and thus makes it impossible to calculate the APR using financial calculators and/or software plus it gives the WRONG ANSWER! Try to calculate the APR for this Bank example using their numbers as follows: Whether that is 3.315% or 0.03315 %, it really does not matter because both are far from the Bank’s 3.03% as advertised. A further point of concern is that , my APR software calculation of 3.0256% calculates the 48 month outstanding balance closer than the Banks APR of 3.03%, which would calculate a balance at 48 months of $177,119. Most reasonable people would not fret over a 52 cents difference in the practical world of mortgages, when talking about hundreds of thousands of dollars. However it should be said that the results of some mortgage calculations (read: especially calculations based upon algebraic exponents) are very sensitive to the number of decimal places used and on which financial calculator you are using!

|

amortizationdotcom Mortgage Calculator for iPhone Introduction to Canadian and American Mortgages Seminar on prepaying principal (Part A) Seminar on prepaying principal (Part B) Global TV Interview regarding 40 Year Mortgages

Look for this logo on the Apple Store!

|

||||||||||||||||||||||||||

<

Go Back |

{kind=link}