|

amortization.com Ltd. 905-639-0374

|

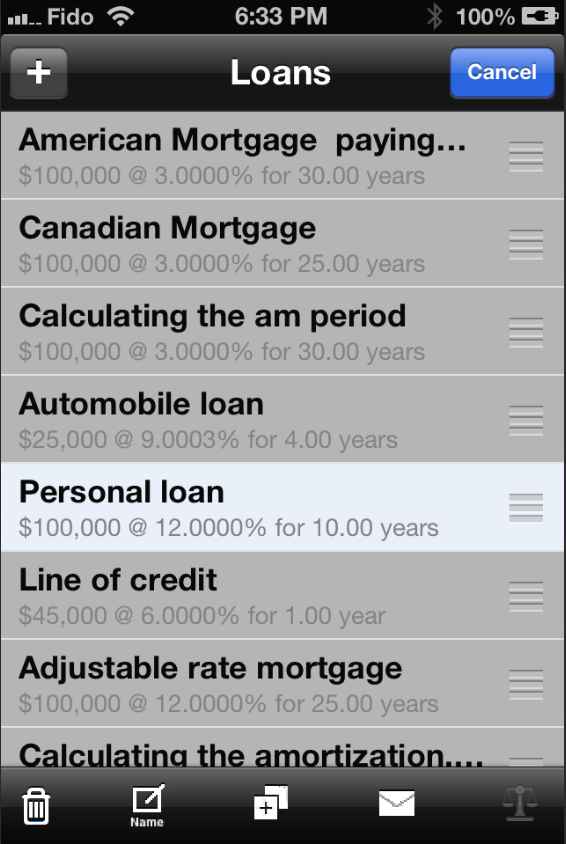

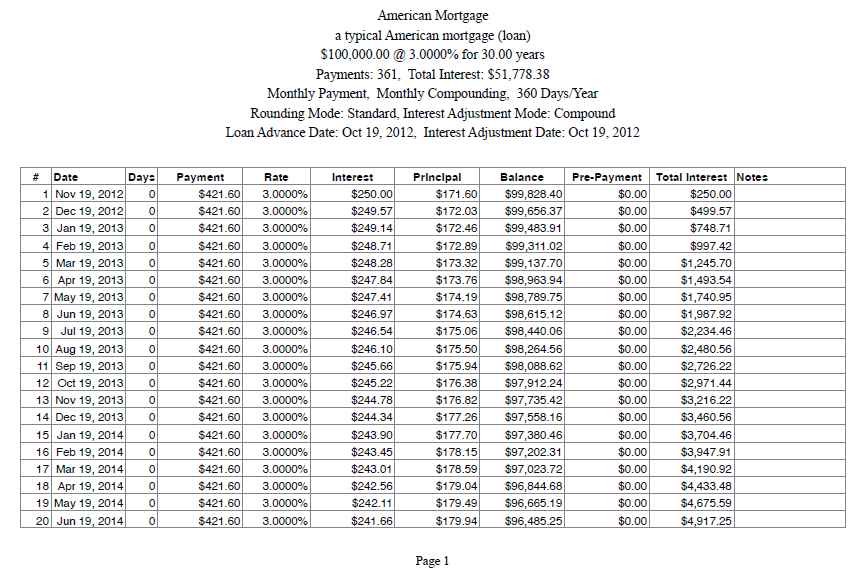

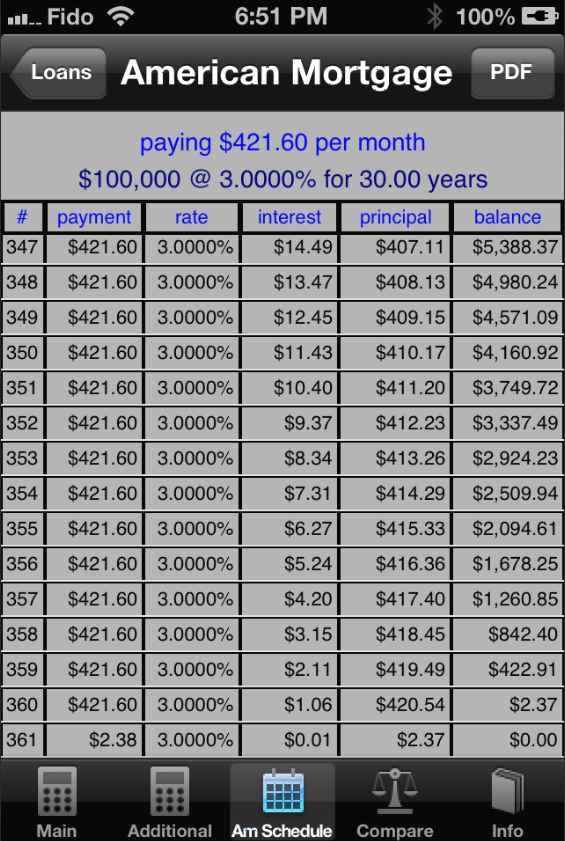

COMING SOON When you borrow money the first thing you ask for is an amortization schedule. An amortization schedule is a financial roadmap showing you the breakdown of the blended payments and the balance owing after each payment. Amortization schedules for automobile loans, personal loans and mortgages are all calculated the same way. A mortgage is just a special name for a loan when your house is used as collateral. From this point on all references will be for a loan, regardless if it’s a house, automobile or personal loan. Touching the green amortization icon ($) on the dashboard takes you to the Loans screen. After installing, when you first use the app there will be one loan name on this screen, Untitled. To edit the loan name and description of the initial Untitled name on the Loans screen, you touch the Edit symbol at the top right corner of the Loans screen and then touch the Untitled name which will then be shown with a white background and four icons will appear at the bottom of the screen. Touching the garbage can icon will delete that loan/mortgage information. Touching the Name icon will take you to the Edit Name and Description screen. After changing the loan name and description you can go to the MAIN screen calculator and then enter your specific data which will automatically be saved under that new file name. Touching the two plus squares icon will duplicate that highlighted name and append “Copy” to the end of the name. Touching the envelope icon will allow you to send the amortization schedule, in PDF format, based on that data to any valid email address. Touching the Untitled name will take you to the Main screen, which is the calculator, with initial defaults for a loan (Principal) of $100,000 at 3%, amortized for 30 years with a monthly payment of $421.60. The other defaults are as follows. Monthly payments, Standard rounding and the “Compounding” type is Monthly which is standard for all American loans. If you’re a Canadian user touch the “Compounding” type box and change it to Semi-annual. The data input boxes have black numbers on a white background. The box that is being calculated has red numbers on a grey background. Initially the Main screen is set to calculate the Monthly payment for that Untitled data. To calculate any of the other data boxes (this feature is not available on financial calculators costing a hundred dollars or more), touch the prompt message in front of that box and its colour will change to red. For example, what if you wanted to pay more than the $421.60 monthly payment, say $500 then you would discover the amortization period would be reduced to 23.167 years or 278 monthly payments instead of 361 and saving you almost thirteen thousand dollars. You could also save these two different scenarios under different Untitled names on the Loans screen and compare them on the Compare screen. The information at the bottom of the Main screen show the total interest for the loan as $51,778.38 and requires 361 payments. As can be seen from the Am Schedule screen the last monthly payment is $2.38 one more than the 360 as per the amortization period input box of 30 years. This is a common occurrence because of rounding, do not be alarmed. Touching the Additional icon at the bottom of the Main screen will take you to the Additional screen displaying four additional defaults that can be changed. Interest Adjustment: This determines how the interest is being calculated if the Loan Advance Date (the day you get the money) and the Interest Adjustment Date are different. Days per Year: This determines how the interest for a blended monthly payment amortization schedule is calculated. For example, set on 360 the year is assumed to be divided into 12 equal months and thus for an annual interest rate of 12% the monthly interest factor is CONSTANT each month at 0.01 that is 0.12/12 = 0.01 The Loan Advance Date and Interest Adjustment Date: If the lender gives you the $100,000 loan at 3% amortized for 30 years on Oct 17th 2012 this is the Advance Date. Usually the lender wants to receive the blended monthly payments on the first of each month. On November 1st the lender asks for an interest payment of $124.92 which is the interest owing for the use of the money for 15 days. In effect the interest payment/adjustment makes Nov 1st the new advance date and thus the first blended payment is due on Dec 1st 2012. EIR%: This is actual interest rate that the lender achieves if the lender lends out (reinvests) each and every payment as he receives to someone else at the same 3% rate.

|

amortizationdotcom Mortgage Calculator for iPhone Introduction to Canadian and American Mortgages Seminar on prepaying principal (Part A) Seminar on prepaying principal (Part B) Global TV Interview regarding 40 Year Mortgages

Look for this logo on the Apple Store!

|

||||||||||||||||||||||||||

<

Go Back |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}