|

amortization.com Ltd. 905-639-0374

|

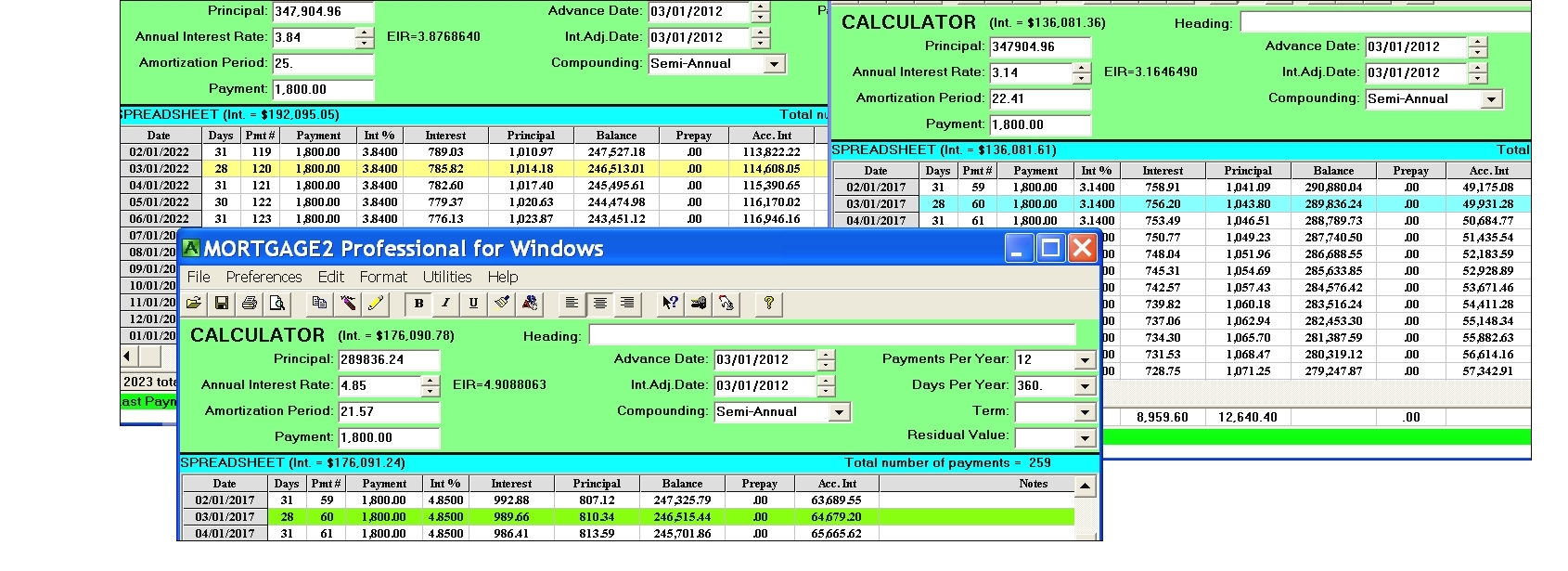

There are two options before you as you deliberate renewing your mortgage, a 10 year 3.84% interest rate or a 5 year 3.14% interest rate. Should you lock in at 3.84% for ten years, for peace of mind, or take the lower five year rate of 3.14% and hope five years down the road the 5 year term rates are the same or lower? Assume you take the five year term rate of 3.14%. How high would the five year term interest rates have to be five years from now to make it the same as if you took the ten year term rate of 3.84%?

Quick Answer: Detailed Answer: The average price of a house in January of 2012 in Canada just reached the $348,000. A 25 year amortization period was chosen and the interest rate is 3.84%. The monthly payment was selected to be an even $1,800 thus the Principal was recalculated to be $347,904.96 (this required the 3 out of 4 calculation feature). After 10 years of $1800 per month payments at 3.84% the total interest paid would be $114,608. So that leaves only $64,677 in interest that can be paid in the second 5 year term if the two 5 year terms are to extract the same interest as the 10 year term (114,608 – 49,931 = 64,677). By playing the “what if” game with the 3 out of 4 feature (starting with a rate of 3.14%) the rate in the CALCULATOR was increased and the Amortization Period was recalculated until the accumulated interest in the SPREADSHEET came close to $64,677. CONCLUSION:

|

amortizationdotcom Mortgage Calculator for iPhone Introduction to Canadian and American Mortgages Seminar on prepaying principal (Part A) Seminar on prepaying principal (Part B) Global TV Interview regarding 40 Year Mortgages

Look for this logo on the Apple Store!

|

||||||||||||||||||||||||||

<

Go Back |

{kind=link}