|

amortization.com Ltd. 905-639-0374

|

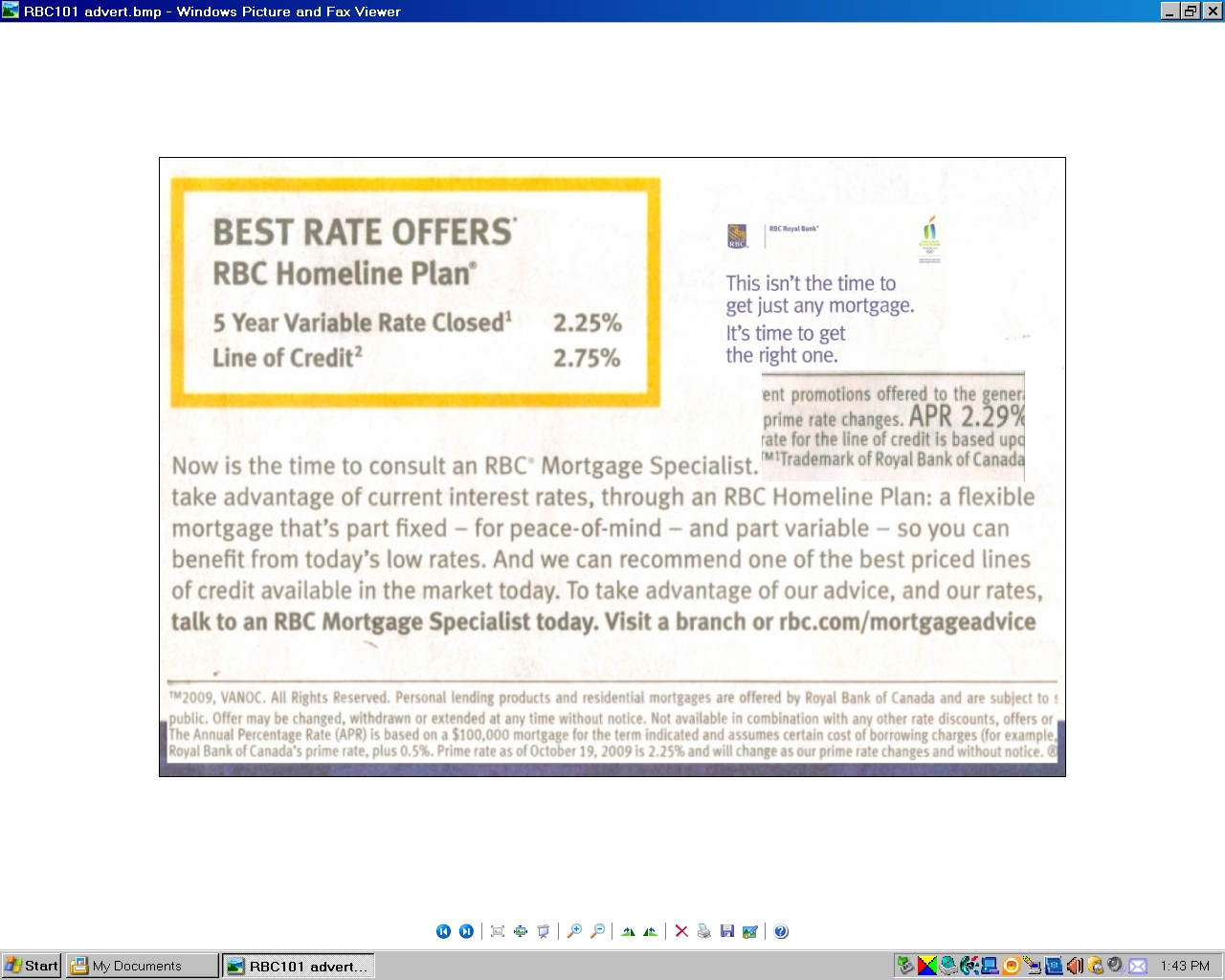

Canada’s largest Bank, RBC Royal Bank prides itself as a “Proud Presenting Partner of the Vancouver 2010 Olympic Torch Relay”. I only wish the RBC and the other major Canadian banks would pride themselves in providing meaningful and easy to understand financial information concerning mortgages in addition to all their “do good marketing” efforts. Many recent full page newspaper advertisements by the RBC tell readers not to get just “any mortgage” but the time to get the “right one” from RBC is now. Their example of a $100,000 mortgage with a 5 year variable rate, closed mortgage at 2.25% is incomplete and confusing. In the squint print footnote at the bottom of the advertisement RBC quotes an APR of 2.29%. Could this be nothing more than a legal compliance. This advertisement has prompted me to ask all of the major Canadian Banks What exactly does an APR disclose to a borrower and how is this APR calculated? Another reason I ask this APR question is because another area of confusion is the five major Banks have their own way of calculating an IRD early renewal “penalty” even though Canada Mortgage and Housing Corporation outlined a simple, logical method over 25 years ago that the Banks have ignored. Is this current APR calculation just more of the same old same old? In order to answer the APR question the following additional information must be stated in any advertising/calculation concerning a mortgage: ● Cost of borrowing charges (dollar value) How does one calculate an APR when the interest rate could be changing each month? SUGESTIONS:

|

amortizationdotcom Mortgage Calculator for iPhone Introduction to Canadian and American Mortgages Seminar on prepaying principal (Part A) Seminar on prepaying principal (Part B) Global TV Interview regarding 40 Year Mortgages

Look for this logo on the Apple Store!

|

||||||||||||||||||||||||||

<

Go Back |

{kind=link}