|

amortization.com Ltd. 905-639-0374

|

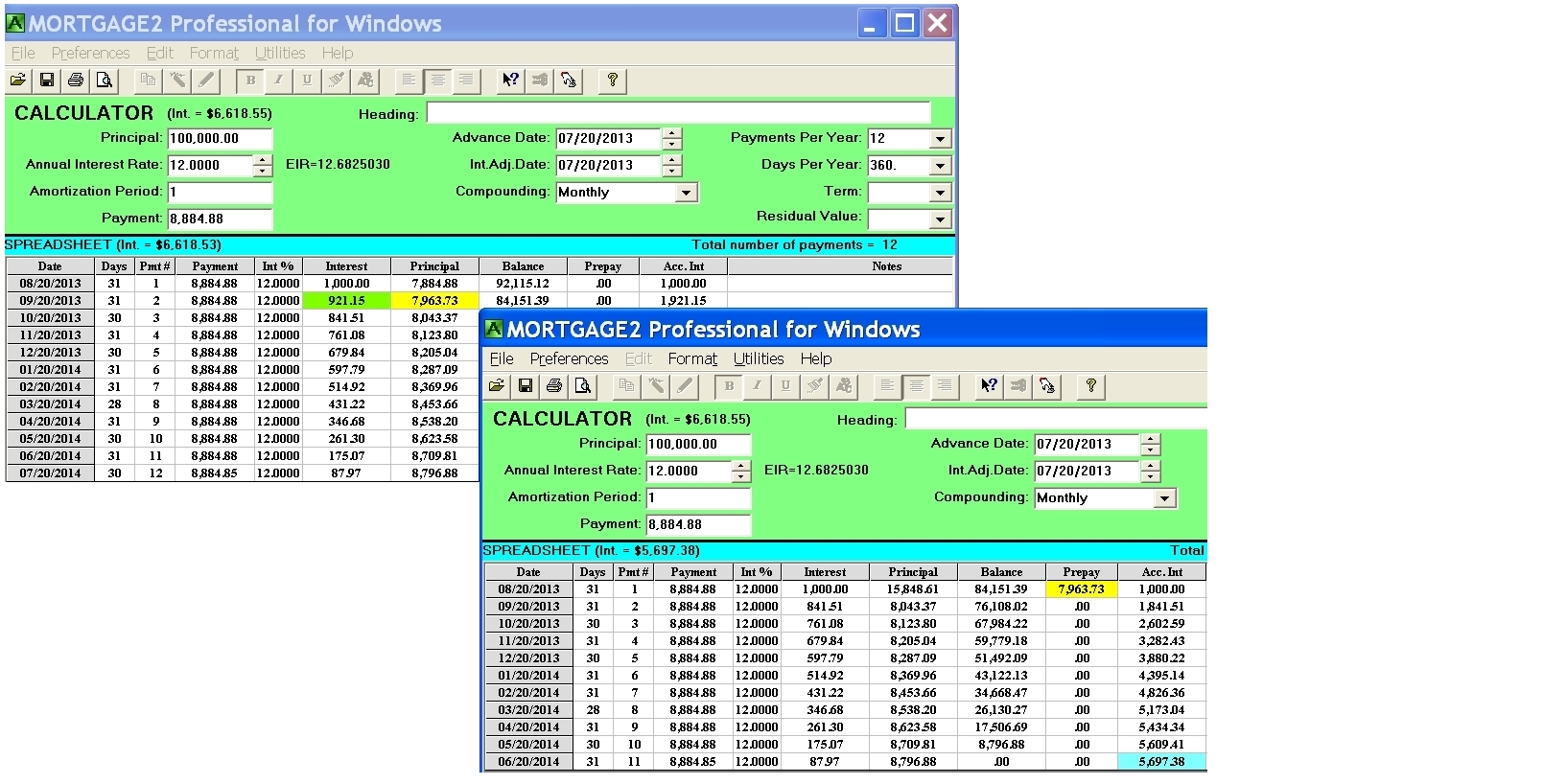

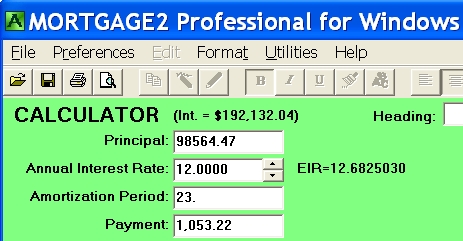

This explanation assumes your mortgage is “open” which means you can pay off principal, or all of it, at any time without penalty. Open mortgages usually charge a higher interest rate. Personal loans and car loans automatically fall into this category. I strongly advise to always prepay principal along with your regularly scheduled payment, because it makes the mathematics simple and clean. If you prepay in mid month or between regular payments the mathematics becomes complicated. If you prepay principal, for an amortized loan or mortgage, each blended payment consists of an interest portion and a principal portion. If you prepay the principal portion of a future blended payment you automatically save the interest portion of that future blended payment. You can also prepay more than one principal portion. For example, assume a 25 year amortization period. If you prepay the 12 principal portions of the next 12 blended payments for the second year of your amortization schedule, along with your 12th blended payment, you save the 12 interest portions of payments 13 to 24. Your amortization period (time to pay off the loan in full) is then reduced to 23 years. In essence the 2nd year of the amortization schedule disappears. You could actually cut out the second year and tape the remainder of the schedule to the first year part. The payment numbers will be out of wack but the rest of the schedule is mathematically intact and you do not need another amortization schedule. The new principal balance owing is the balance after the 12th normal payment minus the total of the 12 principal prepayments. (Figure 1) shows a $100,000 loan at 12% amortized for one year. If you prepaid the principal portion of the second payment ($7,963.73) along with the 1st payment you would save $921.15 in interest and reduce the total number of payments to 11 instead of 12. You can also do this on your iPhone (Figure 1a) with Version 2 of amortization.com on Apple's iTunes. (Figure 2) shows a $100,000 loan amortized for 25 years and the highlighted blended payments for the second year, and their totals for the second year at the bottom of the screen. The principal portions (in yellow) of the blended payments for the second year add up to $760.57 If you pay the $760.57 along with the 12th payment you save $11,878.07 in interest over the next 23 years. (Figure 3) is proof that the amortization schedule reduces to 23 years. Once you grasp this concept you will ask yourself why lenders are not in a hurry to inform you about this technique!

|

amortizationdotcom Mortgage Calculator for iPhone Introduction to Canadian and American Mortgages Seminar on prepaying principal (Part A) Seminar on prepaying principal (Part B) Global TV Interview regarding 40 Year Mortgages

Look for this logo on the Apple Store!

|

||||||||||||||||||||||||||

<

Go Back |

{kind=link}

{kind=link}

{kind=link}

{kind=link}